With so many types of insurance available, it’s natural to question whether an umbrella policy is a worthwhile expense. In fact, many people ask, is an umbrella policy a waste of money?

While it may appear optional or redundant at first glance, an umbrella policy provides crucial, added protection that can prevent serious financial loss.

This article explores why, for most people, an umbrella policy is far from a waste—it’s an affordable way to safeguard assets, cover unexpected costs, and provide peace of mind.

What is an Umbrella Policy?

First, let’s answer what is an umbrella policy. An umbrella policy offers additional liability insurance that goes beyond the limits of standard home, auto, or even boat policies. Unlike primary insurance, which has limits and conditions, an umbrella policy extends these limits to cover costs that your regular insurance won’t. This can include personal liability costs associated with injury, property damage, and certain lawsuits, such as defamation. In essence, an umbrella policy is a safety net designed to protect your financial assets from large, unexpected claims.

For example, if you’re involved in a major car accident where medical expenses and damages exceed your auto insurance’s liability limit, an umbrella policy would step in to cover those costs. It can also cover legal fees if you’re sued for something like libel or slander. This kind of extensive coverage is essential for protecting personal assets from serious claims that could otherwise lead to financial ruin.

Is an Umbrella Policy a Waste of Money?

The short answer is no; an umbrella policy is not a waste of money. While it might seem like an extra expense, especially if you already have primary insurance, it’s one of the most affordable ways to protect against high-cost lawsuits or claims.

For individuals with significant assets, multiple properties, or family members on the policy, the extra layer of liability coverage can be invaluable.

Even for those without extensive wealth, umbrella insurance offers excellent protection that, in the event of a large claim, your financial future remains secure. In reality, this policy type is a smart, forward-thinking way to manage financial risk.

How Umbrella Insurance Works

An umbrella policy “sits on top” of your existing insurance, meaning it activates only after your primary policy limits are exhausted. If you’re involved in an accident with damages that exceed your auto or home insurance limits, an umbrella policy covers the remainder, up to its own limit. This supplemental nature is what makes it so effective: it’s there to protect you when primary insurance is no longer enough.

In addition to this coverage, umbrella policies often include broader liability protection, such as covering legal fees or certain claims like defamation or false arrest that standard insurance won’t cover. This expanded scope makes an umbrella policy unique and valuable, offering peace of mind at a reasonable cost.

Cost vs. Benefit of Umbrella Insurance

Umbrella insurance is surprisingly affordable, especially considering the extensive protection it provides. Most policies with $1 million in coverage cost between $150 and $300 annually, and additional millions of coverage can be added for a small increase in premium. Compared to the financial risk of a significant liability claim, this is a relatively low cost for a very high benefit.

An umbrella policy protects against devastating financial loss, which is why it’s such a worthwhile investment. For those with valuable assets to protect, the small annual premium is a minimal price to pay for substantial peace of mind. Even in less extreme cases, the cost of an umbrella policy is often far outweighed by its ability to protect against unforeseen liabilities, making it a smart financial decision.

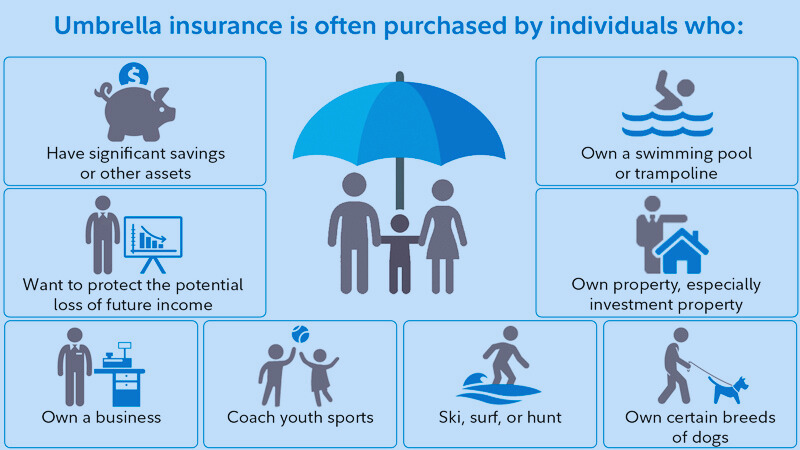

Who Should Consider an Umbrella Policy?

While everyone benefits from an extra layer of security, certain individuals have more reason to consider an umbrella policy. High-net-worth individuals, for example, have more to lose and often face greater liability exposure. Those with rental properties, recreational vehicles, or additional properties can also benefit from umbrella coverage, as they often face risks that aren’t fully covered by standard insurance.

Even those without large assets may want umbrella insurance if they engage in high-liability activities, like hosting guests frequently or owning a dog that might pose a risk. An umbrella policy is a wise choice for families with teenage drivers, as it helps protect against potentially costly auto-related claims. For these individuals, the question “is an umbrella policy a waste of money?” often becomes irrelevant. Instead, it becomes a practical investment to secure one’s financial future.

Common Misconceptions about Umbrella Policies

An often misconception is that umbrella insurance is unnecessary, assuming that other policies offer enough protection. However, standard insurance policies are limited, often covering far less than what may be needed in a high-liability situation. Umbrella insurance steps in only when these policies fall short, covering larger claims and offering unique protections for certain types of liability not addressed by home or auto policies.

Additionally, many assume that umbrella insurance is prohibitively expensive, but it’s usually quite affordable. This misconception often leads people to forgo valuable coverage, putting them at risk in the event of a high-cost liability claim. By understanding its affordability and extended coverage, it’s clear that umbrella insurance is a worthwhile addition rather than an unnecessary expense.

When an Umbrella Policy Might Not Be Necessary

Though umbrella insurance is valuable for many, there are cases where it might not be essential. For individuals with limited assets, low-risk lifestyles, or no family members dependent on them, an umbrella policy may feel unnecessary. However, this doesn’t mean it’s a waste of money—only that it may not be as urgent a priority as it is for those with higher net worth or risk exposure.

In some cases, simply increasing the liability limits on home or auto insurance might provide sufficient coverage. Still, these options should be weighed carefully, as umbrella insurance covers additional liabilities that standard policies don’t. For those who want peace of mind against any eventuality, an umbrella policy is an affordable, reliable way to secure comprehensive coverage.

Risks of Not Having an Umbrella Policy

Without umbrella insurance, individuals with significant assets or risk exposure could face serious financial consequences. In the event of a major lawsuit or claim that exceeds standard policy limits, out-of-pocket costs could lead to debt, asset liquidation, or even bankruptcy. For those in high-risk scenarios, such as landlords or frequent travelers, the lack of this added coverage could mean financial devastation in the event of an accident or lawsuit.

Additionally, umbrella insurance covers unique liabilities, such as defamation or false arrest, which are often not addressed by standard policies. Without this protection, individuals may find themselves vulnerable to large claims, even if they’ve done nothing wrong. Having an umbrella policy ensures that no matter the situation, you’re protected against unexpected liability risks.

How to Decide if an Umbrella Policy is Right for You

Choosing whether to invest in an umbrella policy involves evaluating personal assets, lifestyle, and exposure to liability. Those with substantial savings, investments, or property should consider umbrella coverage as a safeguard against potential asset loss. Additionally, lifestyle factors, such as owning a business, rental property, or frequently hosting guests, all increase the chances of a liability claim, making umbrella insurance more essential.

Consulting an insurance advisor can help you understand how umbrella insurance fits into your overall financial plan. With expert advice, you can make an informed decision about whether this policy will meet your unique needs. For most people, an umbrella policy offers invaluable protection, making it a prudent choice rather than a waste of money.

Conclusion

In conclusion, an umbrella policy is far from a waste of money. Instead, it’s an affordable way to secure long-term financial stability against large liability claims or lawsuits. By extending coverage limits and protecting assets in ways that standard policies cannot, umbrella insurance offers peace of mind and substantial security for those who need it most. When asking, “is an umbrella policy a waste of money?” it’s clear that the answer is no—it’s a wise investment in personal and financial protection.

Additionally, for insurance agencies managing large client bases and complex workloads, insurance outsourcing services can ease the administrative burden, helping agencies stay efficient and focused on providing excellent client service. Through outsourcing, agencies can better meet clients’ needs, such as recommending and managing umbrella policies for comprehensive asset protection.